Once sealed by ice, the Arctic is gradually opening to ships, energy projects, and renewed great power competition. Shorter routes promise savings, untapped resources attract investment, and geopolitical interests are beginning to overlap in a region long defined by isolation.

- Access: shrinking summer ice opens seasonal routes

- Shipping and scale: most traffic is regional; Suez and Panama still dominate

- Signals to watch: longer seasons, stronger cable protection, China and Greenland’s role

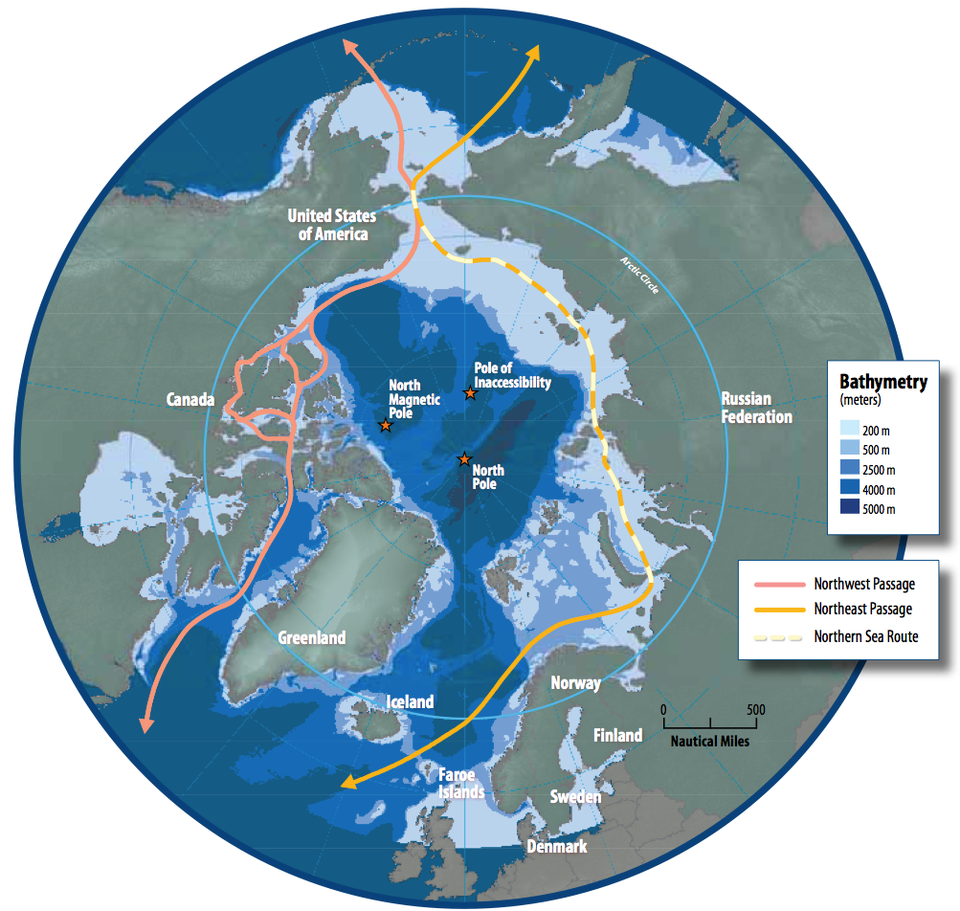

Arctic Shipping: Potential and Limits

Retreating sea ice has created seasonal shipping windows along Russia’s Northern Sea Route. Traffic is increasing, but only a small share consists of full Asia-to-Europe transit. Most voyages support regional energy and mining projects. On certain routes between Northern Europe and East Asia, the Arctic shortcut can reduce distance by 30–40% and cut travel time by roughly two weeks during favorable conditions. The main sailing window, however, usually runs from July through November, and unpredictable ice and weather still limit schedule reliability. The Suez Canal therefore continues to carry a large share of global trade. In practice, Arctic shipping functions as a seasonal supplement rather than a replacement.

For scale, the Suez Canal still carries about 12–15% of world trade, while the Northern Sea Route’s 2023 cargo included about 2.1 million tons of true transit, out of 36.254 million tons in total. For the bigger picture on global trade, see global trade balances.

Arctic Resources and Investment

The Arctic holds significant undiscovered oil and gas reserves, much of them offshore. A USGS appraisal estimates about 90 billion barrels of oil and 1,669 trillion cubic feet of natural gas may still be found. At current consumption levels, this would equal roughly two and a half years of global oil demand and about a decade of gas.

This explains the development of LNG hubs such as Yamal. An LNG hub is a large terminal where gas is liquefied or received, stored, and loaded onto ice-class ships for export. Yamal operates as a staging point, moving cargo to transshipment hubs serving both Europe and Asia. New projects face sanctions, high costs, limited insurance, and the need for specialized vessels, making Arctic energy development capital-intensive with long payback periods.

Climate Change and Environmental Rules

The Arctic is warming faster than the global average, reducing summer sea ice and extending seasonal access for shipping and exploration. Weather conditions, ice movement, and safety risks still define operational limits. A ban on heavy fuel oil in Arctic waters began in 2024, but exemptions remain in place until 2029, meaning the transition to cleaner fuels will take time.

Indigenous communities, including in Greenland, often oppose large projects on environmental and cultural grounds.

Security and Governance in the Arctic

With Finland and Sweden now in NATO, seven of the eight Arctic states are alliance members. Priorities increasingly include surveillance, logistics, search and rescue, and the protection of seabed cables and pipelines. These cables carry the majority of intercontinental internet traffic, making disruption both an economic and security risk. The Arctic Council paused cooperation with Russia in 2022; limited projects without Russian participation resumed later that year.

Greenland’s rare earth minerals and its location keep it in U.S. focus, adding to Arctic geopolitical competition.

Russia’s modernized Northern Fleet and Arctic air bases have increased NATO attention on regional security.

China’s Polar Silk Road

China describes itself as a near-Arctic state and includes northern shipping routes within its Polar Silk Road strategy. It holds stakes in Russia’s Yamal LNG project and operates the Yellow River research station in Svalbard. Chinese interests lie in scientific research, natural resource access, shipping routes, and maintaining a long-term strategic presence in the region.

For more on how this fits into China’s infrastructure strategy, see the Belt and Road Initiative.

The Bottom Line for Arctic Geopolitics

The Arctic is opening, but slowly. Ice, weather, and cost still determine when ships move and where investment flows. The region can shorten selected voyages and add seasonal capacity, yet it will not replace the Suez or Panama canals that carry most global trade. The main signals to watch are the length of the sailing season, the security of undersea infrastructure, and the direction of long-term investment. Together, these factors will guide the pace of Arctic shipping, resource development, and geopolitics in the years ahead.

Explore more related deep dives on finance, geopolitics, and power:

- The Logic of the Petrodollar

- BRICS vs G7: Who Holds the Power?

- The Shift to a Multipolar Payments System

- Taiwan as a Geopolitical Chokepoint

Strategy wins when you separate signal from noise.