Artificial intelligence is now the largest driver of market optimism in the United States. Much of today’s economic growth depends on AI infrastructure, yet the money flowing into the sector still far exceeds the money coming out. Companies, investors, and governments are expanding capacity based on hopes for future payoffs, and the distance between belief and real earnings continues to grow.

AI Now Drives Growth, But Mostly on Assumptions

AI investment now makes up roughly 40% of US GDP growth. Just a handful of mega-cap tech companies drive half of the market’s annual gains, mainly through chip demand, rapid data center build-outs, and expectations of future AI revenue. Put simply, their valuations rest more on projected adoption than on today’s earnings.

Spending and Borrowing Have Outrun Real Revenue

From 2024 to 2025, major cloud providers spent more than $560 billion on chips and data centers. JPMorgan estimates that $1.2 trillion in investment-grade corporate debt is now linked to AI companies, making AI the biggest category in the corporate bond market. Yet AI services brought in only about $35 billion during that period as consumers mostly use free tools. For these investments to pay off, paid adoption would need to grow far more quickly.

The Productivity Gains Have Not Arrived Yet

Despite the high expectations, most of the US economy has not yet seen clear productivity gains from AI. Most companies are still running pilot programs, and many have not integrated AI into daily operations. This leaves a widening gap between the cost of building AI capacity and the income needed to sustain it.

Companies Are Buying Hardware Defensively

A major driver of spending is defensive behavior. Companies buy chips so competitors cannot, which inflates demand signals and pushes others to follow even without profitable uses for the hardware. The race is turning into stockpiling GPUs rather than generating sustainable earnings.

GPUs sit at the center of both the boom and the risk. They secure many of the loans funding the buildout, yet they lose value fast. The Nvidia H100, once rented at $8 per hour, now rents for about $1. Many units sit unused because data centers cannot secure enough power, and some power connections take years to approve. Chips age in warehouses, losing value before they do real work. Unlike the fiber laid during the dot-com era, none of this turns into durable capacity.

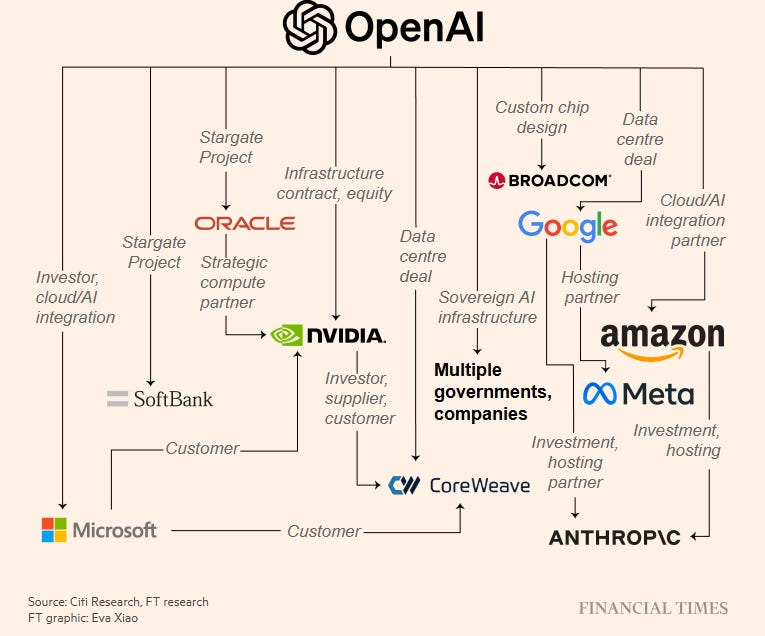

Circular Money Flows Inflate the Apparent Scale

Much of the spending inside the AI ecosystem moves in circles. AI labs rent compute from cloud providers. Those providers borrow billions to buy chips from Nvidia and other manufacturers. In turn, some chip makers and hyperscalers invest directly in the same labs, helping them pay for computing they could not otherwise afford. Suppliers, lenders, and customers often end up being the same few companies.

Case in point: In September 2025, Nvidia announced plans to invest up to $100 billion in OpenAI as part of a data center buildout. OpenAI does not generate the revenue needed to fund hardware at this scale, so Nvidia’s investment helps OpenAI buy the very GPUs Nvidia makes. Nvidia then books that spending as revenue. Part of the demand for Nvidia’s chips is financed by Nvidia itself, while OpenAI expands with capital it could not obtain through normal earnings.

This creates a fragile chain of interdependence. Chip makers rely on AI labs to stay solvent. AI labs rely on cloud providers for affordable compute. Cloud providers rely on debt markets to fund their expansion. Each link assumes the others keep holding up.

Hidden Debt, Public Exposure, and Private Credit

A large share of new data center debt never appears on corporate balance sheets. Companies use special-purpose vehicles, separate entities created to borrow and build facilities, while the parent company later “rents” the finished center through long-term contracts. This does not reduce risk. It only hides it, making it harder for investors to see how much leverage supports the boom.

Utilities and local governments are also taking on major obligations, from building new power lines to guaranteeing electricity supply, all based on the assumption that future AI revenue will eventually justify today’s costs.

“Public funding opens the door; private credit fills the room.” — Stijn McAdam

More AI infrastructure is now financed through private credit funds that lend money at higher rates than traditional banks. These funds manage retirement accounts, insurance pools, and long-term savings for millions of people. When they charge double-digit interest, it signals they see real risk of default.

AI Must Deliver Trillions Soon

Everything now rests on one outcome: AI must generate real revenue fast enough to support the scale of the buildout. The industry needs trillions in new earnings over the coming years for today’s spending to make financial sense. If that revenue arrives, the investment wave could still pay off. If it does not, the loans, leases, and cross-investments holding the system together begin to strain. At that point the sector starts to resemble a market propped up by rising asset prices rather than cash flow. This links back to the broader race toward superintelligence, where rapid progress increases both the opportunity and the fragility. Optimism may still prove right, but the current financial structure leaves little room for slow adoption.

Explore more deep dives connected to AI, chips, and the systems behind our technological future:

- AI, AGI, CGI Made Clear

- The Future of Governance in a Technocratic World

- The Promise and Threat of Quantum Computing

- The US–China Tech Race

Break free from the habits that own you.