Monetary systems rarely collapse overnight. The groundwork for change is usually laid in the background. The visible shift tends to arrive during moments of crisis, when the public is too busy dealing with the fallout.

What we are seeing today goes beyond a routine reform of money. A fully digital financial architecture is steadily coming together, and the tempo is picking up. Currency, identity, assets, and data are moving onto the same rails. Many of the pieces have existed for decades, but their integration now appears to be accelerating.

Centralizing the Money

In 1913, the United States passed the Federal Reserve Act, creating the Federal Reserve system. The stated goal was financial stability after a series of banking crises.

Monetary authority moved from a largely decentralized banking environment into a coordinated central banking structure. Concentrating monetary power in a single institution was, unsurprisingly, presented as “stability.”

Photo: Board of Governors of the Federal Reserve

Europe had already experimented with similar systems through powerful banking houses and sovereign debt networks. We explored this model in How the Rothschilds Enabled Modern Finance.

The logic? Control the issuance of money and credit, and you influence the direction of entire economies.

Then came the perfect validation mechanism: war. The First World War required enormous government borrowing and centralized credit expansion. Large-scale conflict demonstrated something useful to policymakers. Centralized monetary systems make it far easier to finance extraordinary levels of debt. Wars, it turns out, are easier to fund when you control the printing press.

In 1933, President Franklin D. Roosevelt issued Executive Order 6102, forcing Americans to surrender most privately held gold to the government. Shortly after, the official gold price was raised from roughly $20 to $35 per ounce.

In other words, the public handed over the gold, and the government immediately revalued it higher. A neat trick if you can pull it off.

Former U.S. president Franklin Roosevelt signing Executive Order 6102.

Global Institutions

By the end of the Second World War, policymakers believed a coordinated monetary system was necessary to support reconstruction and international trade.

In 1944, representatives from 44 nations met at Bretton Woods to design the postwar financial order. The agreement established the U.S. dollar as the central currency of the global system, convertible into gold for foreign governments and central banks.

Two major institutions were created alongside it.

The International Monetary Fund was tasked with stabilizing currencies and providing emergency lending to countries facing financial crises. The World Bank focused on reconstruction and development lending. With conditions attached, naturally.

On paper, the system was cooperative. In practice, global financial coordination was placed within a relatively small circle of institutions.

Behind the scenes, another organization quietly facilitated cooperation among central banks themselves: the Bank for International Settlements. The BIS is often described as the central bank of central banks. It rarely appears in headlines. Which, if you are coordinating global monetary policy, is probably ideal.

The Bank for International Settlements in Basel, Switzerland.

Photo: Central Banking Publications

Removing the Constraint

By the late 1960s, the Bretton Woods system was under strain. The United States had issued far more dollars abroad than it held in gold reserves to redeem them. Foreign governments began requesting gold in exchange for their dollars.

So, you guessed it. In 1971, President Nixon ended dollar convertibility into gold. From that moment forward, the global monetary system operated entirely on fiat currency. Money backed primarily by confidence. Well, and the occasional aircraft carrier.

Soon afterward, the petrodollar arrangement ensured that global oil trade remained priced in U.S. dollars, preserving worldwide demand for the currency.

The constraint had been removed. Credit expansion could now accelerate far beyond what a gold system would allow. And accelerate it did.

President Nixon announces the end of gold convertibility, 1971

Photo: Richard Nixon Library

Financialization

Over the following decades, finance grew dramatically in both scale and complexity.

Debt markets expanded. Derivatives multiplied. Asset prices became a central concern of economic policy. By the early 2000s, financial markets had grown so large that governments increasingly reacted to their movements rather than guiding them.

The 2008 financial crisis exposed how fragile that system had become.

Central banks responded with unprecedented measures. Through quantitative easing, they created money digitally and used it to purchase vast quantities of financial assets.

Markets became increasingly dependent on central bank support. Finance had entered the digital age, though money itself remained conceptually simple. Numbers recorded in bank ledgers.

The next step goes much further.

Programmable Money

Digital banking already exists. But programmable money introduces a different capability.

A Central Bank Digital Currency (CBDC) is state-issued money designed for the digital environment. Unlike cash, it can be programmed. Transactions can be monitored in real time. Spending restrictions can be coded. Expiration dates can even be attached to money itself.

The BIS (remember them?) has already launched projects testing cross-border CBDC settlement systems, aimed at connecting multiple central banks through shared digital payment infrastructure. Agustín Carstens, former General Manager of the BIS, once remarked that CBDCs could give central banks “absolute control” over money, including the ability to determine how digital currency is used.

Agustín Carstens speaks at BOJ conference, 2025

Photo: Kiyoshi Ota/Bloomberg

And do not be fooled: a stablecoin functions much like a CBDC, except it is issued by a private company rather than a central bank. The difference lies mostly in who operates the system.

This is where the story becomes really interesting.

The Control Grid

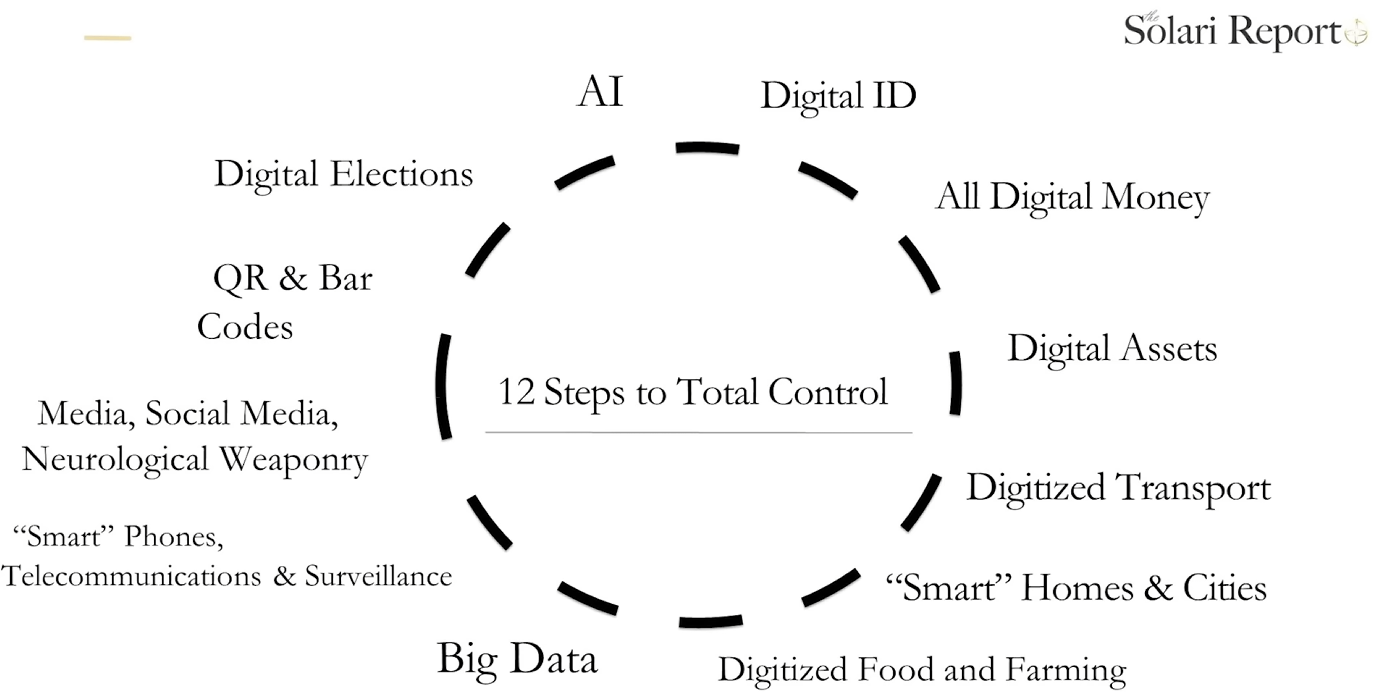

Investment banker and former U.S. public official Catherine Austin Fitts describes these developments as components of a digital control grid. “Many people don’t see it coming because there are many disparate parts,” she noted in an interview. Digital currency alone does not create systemic control. It becomes powerful when connected to other digital infrastructure.

Fitts outlines 12 elements that together enable total control. Artificial intelligence can process vast streams of data from transactions, communications, and physical movement. Digital identification systems connect financial access to verified identity. If all money becomes digital, every transaction becomes traceable.

12 Steps to Total Control.

Photo: The Solari Report

Real-world assets such as homes, vehicles, and licenses can also be tokenized (meaning they are represented digitally on a ledger). BlackRock CEO Larry Fink even stated that “we’re just at the beginning of the tokenization of all assets.”

Transportation networks increasingly rely on digital access systems that record movement. Cities deploy sensors and cameras as part of “smart city” infrastructure. Supply chains use digital tracking systems that follow goods from factory to retail shelf. “You’ll own nothing and you’ll be happy.” Kind regards, the future.

Individually, each development can be presented as modernization or efficiency. Together, they begin to resemble a digital corral.

Catherine Austin Fitts during an interview with Michael Yon, 2026.

The Next Phase

The next financial disruption, whether triggered by excessive debt, geopolitical tension, or a market breakdown, will likely accelerate the shift toward digital monetary systems. When that moment arrives, programmable financial infrastructure will probably be presented as the logical upgrade to the current system.

Fitts emphasizes that individuals are not entirely powerless within this transition. She encourages practical forms of resilience: maintaining access to cash, strengthening trusted local networks, choosing financial institutions that operate with integrity, and continuing independent research through sources such as The Solari Report.

Explore more deep dives connected to finance, tech, power, and the systems behind it: