A bubble grows too large, people get greedy, and eventually the system corrects itself. That is how a financial crash “just happens,” right?

It is a simple and comfortable explanation, but the story usually stops just before it becomes uncomfortable.

The Illusion of the Cycle

Basic economics describes a recurring boom and bust cycle: optimism rises, credit expands, spending increases, asset prices inflate, until reality catches up. The system resets, and the pattern begins again.

The Wall Street Crash of 1929, which ended the “Roaring Twenties” and led into the Great Depression, is often presented as a textbook example. That description is not wrong, but it is incomplete.

If the system runs on credit, and credit can be expanded, why does it ever stop? The answer is found in its structure.

Money as a Construct

Banks do not simply store money; they create it through lending. When a bank issues a loan, it does not transfer existing money – it creates new purchasing power. Deposits increase as debt increases.

Central banks influence this process primarily through interest rates. Lower rates encourage borrowing and expand liquidity, while higher rates restrict it. We explore this further in our analysis The Role of Central Banks.

The Foundation

The modern framework began to form in the late 17th century.

After the Glorious Revolution (1688) shifted power from monarchy to Parliament, the creation of the Bank of England formalized a new model, where governments were financed through debt markets rather than direct taxation alone.

Formation of the Dutch fleet that carried William III to England in 1688.

Photo: Rijksmuseum

From this point onward, a recurring pattern appears: war drives borrowing, borrowing expands credit, credit fuels speculation, and speculation eventually breaks.

For example: the War of the Spanish Succession (1701) → credit expansion → the South Sea Bubble (1720) → collapse → broader credit stress in the decades that followed.

As the British Empire expanded, this model scaled globally. Private capital funded governments, with repayment secured through taxation. Three structural features followed:

1. Profits remain private, while losses can be socialized.

2. Ongoing expansion becomes necessary to sustain the system.

3. Capital operates across borders, reducing national constraints.

Expansion Into America

This framework did not remain in Britain. It took hold in the United States alongside industrial expansion, where capital concentration accelerated in the late 19th and early 20th centuries.

In 1913, the Federal Reserve established a central banking system in the U.S., placing credit management at the core of the economy.

What followed mirrors the earlier dynamic: World War I → credit expansion → asset inflation → the 1929 crash → the Great Depression → World War II.

After World War II, leadership shifted to the United States. The dollar became the center of the system, formalized through Bretton Woods and later reinforced by the petrodollar system.

Institutions such as the International Monetary Fund (IMF), the World Bank, and the Bank for International Settlements (BIS) extended and coordinated this structure globally.

Creation of the Bretton Woods System, New Hampshire, 1944.

Photo: Associated Press

2008 Revisited

While the 2008 financial crisis is often framed as a failure of risk management, it followed the same structural logic.

Low interest rates after the early 2000s recession accelerated mortgage lending. Risky loans were bundled into securities and sold worldwide, spreading exposure across the system while increasing total leverage.

At the same time, some large players used derivatives to take positions that would gain value if those securities failed. When the collapse came, some lost everything and others profited significantly.

As in previous cycles, the collapse redistributed wealth and power, concentrating it where capital was strongest.

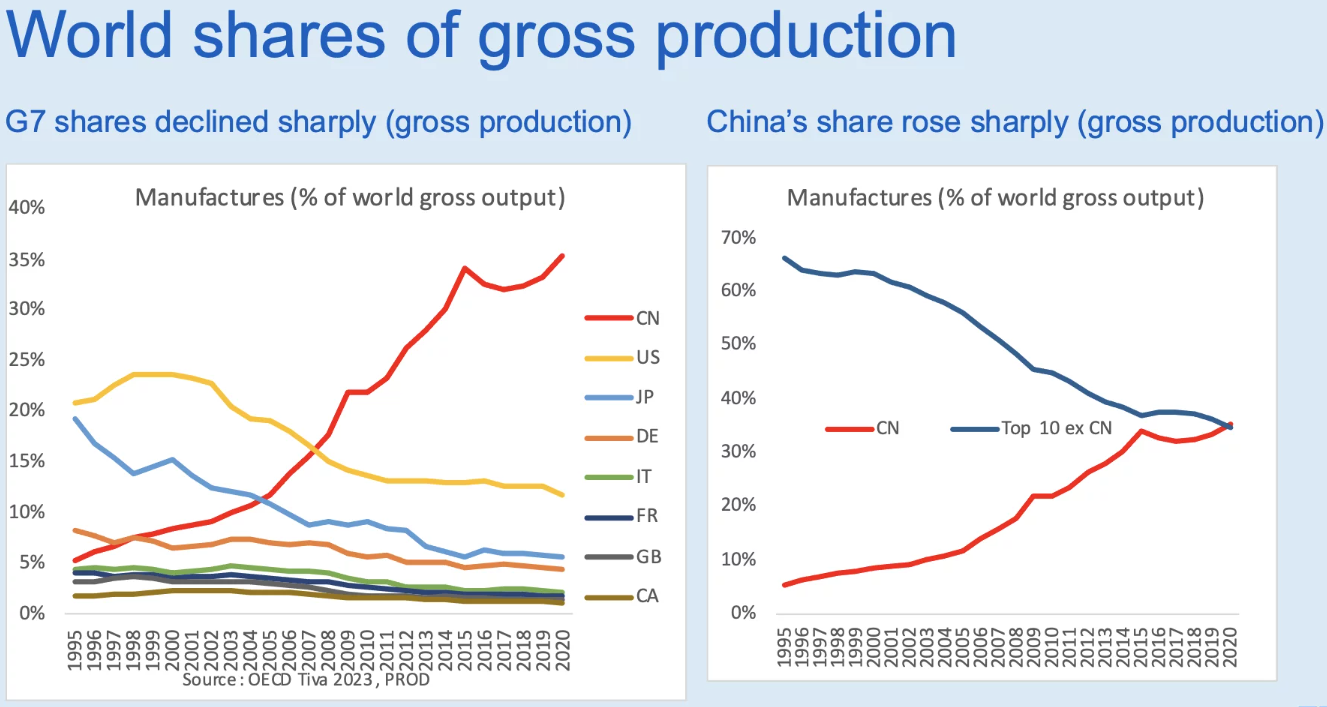

Shifting Gravity

After 2008, growth in Western economies slowed. Meanwhile, production and infrastructure expansion accelerated in China, absorbing a growing share of global demand and capital flows.

China’s meteoric rise in manufacturing.

Photo: OECD TiVA database, 2023 update

Debt levels increased globally, but within the system, debt functions as both asset and liability.

The Next Phase

Today, multiple pressures are building at once: geopolitical conflict, aging populations, record debt levels, dependence on liquidity, overpriced assets, and the AI bubble.

The dollar-based payment system is also under strain. Financial infrastructure is increasingly used as a tool of power, while a shift toward multipolar payment systems points to a gradual redistribution of influence.

Capital continues to search for new areas of expansion. Historically, these transitions are not smooth. If the pattern holds, the next reset becomes a question not just of when, but where the pressure breaks first.

We highly recommend reading our deep analysis about the groundwork being laid for the next collapse: